Refinance Calculator: Should You Refinance Your Mortgage?

Are you considering refinancing your mortgage but are unsure if it’s the right financial move? A refinance calculator can help you evaluate your options and make an informed decision. By using a refinance calculator, you can quickly determine whether refinancing will save you money or achieve other financial goals. In this article, we’ll guide you through everything you need to know about mortgage refinancing and how a refinance calculator can assist you in the process.

What is Mortgage Refinancing?

Understanding Mortgage Refinancing

Mortgage refinancing involves taking out a new loan to replace your existing mortgage. The goal is usually to secure a lower interest rate, reduce monthly payments, shorten the loan term, or access home equity. While refinancing can offer financial benefits, it’s essential to carefully consider the costs and long-term impact.

Key Terms in Mortgage Refinancing

- Principal: The remaining balance on your mortgage.

- Interest Rate: The percentage charged on your loan for borrowing money.

- Loan Term: The period you have to repay the loan, typically 15, 20, or 30 years.

- Closing Costs: Fees associated with processing and closing your new mortgage.

Why Use a Refinance Calculator?

Benefits of Using a Refinance Calculator

A refinance calculator can be a powerful tool in determining whether refinancing is the right decision for you. It helps you compare your current mortgage with a potential new loan by calculating the new monthly payments, interest savings, and break-even point.

How a Refinance Calculator Works

A refinance calculator uses the details of your current mortgage, such as the loan balance, interest rate, and remaining term, to compare them with potential new terms. It factors in closing costs and other fees to provide you with a clear picture of the financial impact of refinancing.

Key Factors to Consider Before Refinancing

Current Interest Rates vs. Your Existing Loan

The main reason homeowners refinance is to take advantage of lower interest rates. However, it’s essential to compare the rate on your existing mortgage with current market rates to determine if the savings justify the refinancing costs.

Loan Term Considerations

Shorter Loan Terms

Refinancing to a shorter loan term, like 15 years instead of 30, can save you significant interest over time. However, this usually results in higher monthly payments.

Longer Loan Terms

If your goal is to reduce your monthly payment, extending the loan term may help, but you could end up paying more interest over the life of the loan.

Refinancing Costs: Closing Fees and Other Expenses

When refinancing, you’ll need to account for closing costs, which typically range from 2% to 5% of the loan amount. These fees can include appraisal costs, loan origination fees, title insurance, and more.

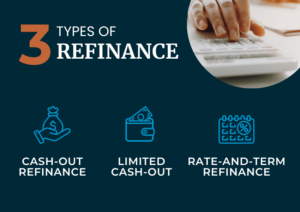

Types of Refinancing:

Rate-and-Term Refinance

This is the most common type of refinancing, where you replace your current mortgage with a new loan at a lower interest rate or for a different loan term.

Cash-Out Refinance

With a cash-out refinance, you take out a new loan for more than you owe on your home and pocket the difference. This is ideal if you need cash for home improvements, debt consolidation, or other expenses.

Streamline Refinance

A streamline refinance is a simplified process offered by certain government-backed loans (such as FHA or VA loans) with less paperwork and lower closing costs, making it a quicker and easier option for homeowners.

Steps to Use a Refinance Calculator

Gather Your Loan Information

Start by collecting all the relevant details of your current mortgage, such as your loan balance, interest rate, remaining loan term, and monthly payment.

Input New Loan Details

Enter the details of the new loan you’re considering, including the loan amount, interest rate, and loan term. Don’t forget to include any closing costs.

Analyze Results and Compare

Once the calculator provides the new monthly payment and interest savings, compare it to your current loan to determine if refinancing is a wise decision. Consider the break-even point to see how long it will take to recoup the closing costs.

Pros and Cons of Mortgage Refinancing

Advantages of Refinancing

- Lower monthly payments if you secure a lower interest rate.

- Reduce total interest payments over the life of the loan.

- Access home equity through cash-out refinancing.

- Shorten the loan term to pay off your mortgage faster.

Disadvantages of Refinancing

- Upfront closing costs, which can be expensive.

- Extending the loan term may lead to paying more interest over time.

- Potentially increasing your monthly payments if you opt for a shorter loan term.

When Should You Consider Refinancing?

Ideal Scenarios for Refinancing

Refinancing is most beneficial when interest rates have significantly dropped, or when you want to switch from an adjustable-rate mortgage to a fixed-rate loan. It can also be an excellent option if you want to reduce your loan term or take advantage of home equity.

Red Flags to Avoid

Avoid refinancing if the closing costs outweigh the potential savings, or if your financial situation could lead to higher rates in the future. Also, be wary of resetting your loan term if you’re already several years into paying off your mortgage.

Using a refinance calculator is an essential step in deciding whether mortgage refinancing is the right choice for you. By comparing your current loan with potential new terms, you can evaluate the benefits, such as lower payments, reduced interest, or cash-out options, and weigh them against the costs. Always consider your long-term financial goals, and consult with a mortgage professional if needed, to make an informed decision.

FAQs

1. How do I know if refinancing is right for me?

If current interest rates are significantly lower than your existing mortgage rate, or if you want to access home equity, refinancing could be beneficial. Use a refinance calculator to determine potential savings.

2. What are the typical closing costs for refinancing?

Closing costs typically range from 2% to 5% of the loan amount, covering expenses like appraisal fees, title insurance, and loan origination fees.

3. Can I refinance with bad credit?

It may be more challenging to refinance with bad credit, but some lenders offer options for homeowners with lower credit scores. Government-backed loans like FHA or VA loans may have more lenient requirements.

4. How often can I refinance my mortgage?

There is no legal limit to how many times you can refinance, but frequent refinancing can lead to high closing costs and reset your loan term, increasing the total interest paid over time.

5. Can I roll closing costs into my new mortgage?

Yes, many lenders allow you to roll closing costs into your new loan, but this will increase the total loan amount and could result in higher monthly payments.

One thought on “Refinance Calculator: Should You Refinance Your Mortgage?”